Strategies to Get Out of Overdraft Without Wrecking Your Budget

In today’s financial landscape, overdrafts are a common hurdle many individuals face. An overdraft occurs when you spend more money than you have available in your bank account, leading to negative balances and often hefty fees. According to a 2023 study by the Consumer Financial Protection Bureau (CFPB), nearly 23 million adults were charged overdraft fees in the past year, with the average fee amounting to $33 per occurrence. Overdrafts can spiral into a cycle of debt, disrupting your budget and causing financial distress. However, with strategic planning and disciplined money management, it’s entirely possible to recover from an overdraft situation without sacrificing your essential expenses or accumulating additional debt.

Understanding how to get back on track involves not only tackling the immediate financial shortfall but also implementing long-term budgeting strategies that prevent repeat overdraft events. This article delves into practical and proven methods to get out of overdraft without wrecking your budget, including real-life examples and a detailed comparison of financial options.

Assess the Situation: Know Your Financial Position Thoroughly

The first step in overcoming an overdraft is to gain a clear and honest understanding of your current financial situation. This means reviewing your bank account statements, identifying all incoming money and outgoing expenses, and pinpointing the exact amount of the overdraft. Many individuals underestimate the severity of their negative balance, which hampers effective decision-making.

For example, Maria, a 29-year-old freelance graphic designer, found herself constantly overdrafting by an average of $150 monthly. Once she began tracking her income flow and expenses meticulously through a budgeting app, she realized that irregular income and non-essential splurges led to these negative balances. Tracking such patterns allows for realistic financial planning that addresses the root cause of overdrafts.

Similarly, Jason, a warehouse manager, used a simple spreadsheet to list his fixed monthly expenses versus discretionary spending. He noted that overdraft fees added another $50 monthly to his budget drain, motivating him to seek alternatives to manage his cash flow better. Knowing exactly where money goes helps avoid optimistic assumptions and creates a practical baseline for debt repayment strategies.

Cut Unnecessary Expenses Without Compromising Essentials

Minimizing expenses is often the quickest way to free up cash for overdraft repayment, but it requires careful distinction between non-essential luxuries and vital costs. A common mistake is to cut back on necessary items such as groceries or utilities, which can backfire by reducing quality of life or causing additional expenses.

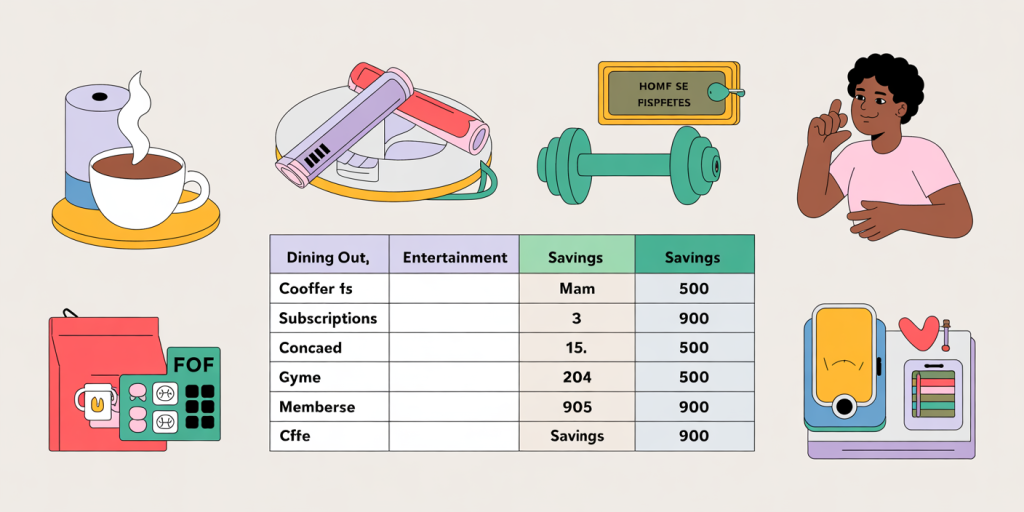

Data from the Bureau of Labor Statistics indicates that Americans spend about 17% of their income on dining out and entertainment. Targeting these areas for cuts can create room in the budget for overdraft recovery without drastic lifestyle changes. For instance, switching from daily coffee shop visits to home-brewed coffee can save approximately $60 monthly.

Practical application can be seen in Chloe’s case, a part-time teacher who reined in her spending by canceling unused gym memberships and limiting online shopping. She allocated the saved funds toward clearing her $300 overdraft within two months. Equally important was renegotiating her cellphone plan from a premium $80 to a budget $40 option, ensuring no burden on her essential communication needs. Using a detailed spending diary helps in making conscious cuts.

The table below highlights average monthly expenses that are commonly adjusted during budget tightening and recommended savings:

| Expense Category | Average Monthly Spend | Suggested Reduction | Potential Savings |

|---|---|---|---|

| Dining Out | $200 | 50% | $100 |

| Entertainment | $120 | 50% | $60 |

| Subscription Services | $50 | 100% (cancel unused) | $50 |

| Gym Membership | $40 | 50% | $20 |

| Grocery Savings | $300 | 10% | $30 |

| Total Potential Savings | $260 |

These savings can be redirected to pay off an overdraft quickly without sacrificing critical needs.

Communicate With Your Bank for Overdraft Relief Options

Banks often provide financial relief options for customers struggling with overdraft balances, particularly if you’re proactive. Contacting your bank can uncover alternatives like temporary fee waivers, overdraft protection plans, or small short-term loans with lower interest rates than penalty fees.

For instance, a 2022 survey by Bankrate revealed that 57% of banks offered at least one form of overdraft assistance to customers who reached out. This shows that many financial institutions prefer retaining customers through support, rather than penalizing them into further distress.

Consider Samantha, who was overwhelmed by $450 in overdraft fees on her checking account. Upon calling her bank, she requested fee reversals and enrolled in a linking service that transfers funds automatically from her savings to cover overdrafts. This not only stopped new fees but also introduced a buffer against future overdrafts.

It is crucial to maintain an honest dialogue. Banks are more willing to aid customers who demonstrate a willingness to manage their finances responsibly. If you anticipate a shortfall, ask about arranging a temporary overdraft limit increase or waiving fees, which can prevent fees from hurting your budget further.

Implement a Structured Repayment Plan to Eradicate Overdraft Debt

Once clear on your financial position and potential relief from the bank, developing a structured repayment plan is vital. Without a scheduled approach, it’s easy to prolong overdraft debt, creating ongoing budget strain.

One method is the “snowball” repayment approach, where you prioritize paying off the smallest overdraft fees and balances first to gain motivation, then tackle the larger amounts. Alternatively, the “avalanche” method focuses on paying the highest-fee overdrafts first, minimizing total costs. Choosing a method depends on personal psychology and financial status.

Timothy’s real case demonstrates this principle: he had multiple overdraft fees totalling $600. Using the avalanche method, he paid off the $50 high-fee overdraft first, which drew his attention and kept him motivated. Completing the larger $400 overdraft soon after was easier because he had eliminated high-cost debts first.

Automating payments via online banking helps maintain discipline in repayment schedules. Even small fixed transfers of $25 weekly can clear overdraft balances in a matter of months, avoiding additional penalties.

| Repayment Method | Description | Pros | Cons |

|---|---|---|---|

| Snowball | Pay smallest debt first | Builds morale fast | May incur more interest overall |

| Avalanche | Pay highest fee balance first | Saves money on fees | Requires discipline |

| Fixed Increment | Set amount paid regularly | Ensures steady progress | May take longer if amount is low |

Choosing and adhering to a plan ensures overdraft does not continue harming your budget.

Boost Income and Emergency Savings to Prevent Future Overdrafts

While cutting costs is effective short-term, increasing income and building an emergency fund safeguard against future overdrafts. Having a financial cushion ensures unexpected expenses do not derail your budget or force costly overdrafts.

Data from the Federal Reserve shows that 36% of Americans cannot cover a $400 emergency without borrowing, indicating a lack of savings that directly contributes to overdraft occurrences. Starting even a small emergency fund, such as $500, can substantially reduce reliance on overdrafts.

Side gigs, freelancing, and selling unused goods on platforms like eBay or Etsy can provide supplementary income streams. For instance, Alex, a delivery driver, augmented his paycheck by $300 monthly through weekend rideshare driving, which he funneled into emergency savings and overdraft repayment.

Automatic transfers from checking to savings, even as low as $25 per paycheck, create a disciplined savings habit without major lifestyle impact. Over time, this buffer prevents overdrafts stemming from delayed income or unforeseen bills and contributes to financial stability.

Looking Ahead: Building Resilience Against Overdrafts

The path to overcoming overdraft challenges is not solely about recovery but adopting a mindset and practices that prevent recurrence. Financial resilience requires continuous monitoring of cash flows, regular budgeting reviews, and adaptability to changing circumstances.

Technological advances offer new tools, such as AI-driven budgeting apps that alert users before their balance drops below zero, effectively preempting overdraft events. According to a 2024 report by Deloitte, 42% of financial app users have avoided overdrafts due to real-time alerts and predictive budgeting features.

Moreover, ongoing financial education plays a crucial role. Individuals who engage in periodic financial literacy programs report greater confidence in managing money and reduced overdraft rates. Initiatives at community centers, workplaces, and online courses can reinforce prudent financial behaviors.

Banks might further innovate with zero-overdraft-fee accounts or low-cost overdraft lines of credit, shifting the financial ecosystem towards fairness and consumer empowerment.

In summary, overcoming overdraft requires a strategic blend of immediate action, disciplined repayment, expense management, and income augmentation. By leveraging available bank assistance, thoughtful budgeting, and emergent technologies, anyone can reclaim financial control without wrecking their budget. Building for the future involves making sustainability and resilience foundational elements of your financial plan, ensuring overdrafts become a thing of the past rather than a recurring hardship.