Financial Literacy for Beginners: Building a Strong Foundation for Your Financial Future

In today’s fast-paced and increasingly complex world, financial literacy is no longer optional—it is essential. Whether you are just starting out in your career, managing a household budget, or planning for future investments, understanding the fundamentals of personal finance empowers you to make informed decisions and secure financial stability. Despite its importance, according to a 2022 survey by the National Financial Educators Council, nearly 60% of adults in the United States rate their financial knowledge as “poor” or “fair,” underscoring the critical need for foundational education in this area.

This guide aims to demystify financial literacy for beginners, providing practical advice, real-life examples, and actionable steps to help you gain control over your finances. By mastering these basics, you can avoid common pitfalls, leverage opportunities wisely, and build a path toward long-term wealth.

—

Understanding the Basics: What Is Financial Literacy?

Financial literacy refers to the ability to understand and use various financial skills, including personal financial management, budgeting, and investing. It encompasses knowledge about how money works, strategies for effectively managing income and expenses, understanding credit, debt, and savings, and making prudent financial choices.

For example, a college graduate who understands how to budget their salary and avoid high-interest credit card debt is practicing financial literacy. Conversely, without these skills, it’s easy to fall into debt, miss payments, or miss investment opportunities.

Statistics reveal a direct correlation between financial literacy and financial well-being. A 2023 survey conducted by FINRA Investor Education Foundation found that individuals with high financial literacy scores were 70% more likely to save for emergencies and retirement. This demonstrates that foundational financial knowledge can greatly improve one’s fiscal security and overall quality of life.

—

Budgeting: The Cornerstone of Financial Control

An essential step for beginners is creating and maintaining a budget—a plan that tracks income versus expenses. Without a budget, it is nearly impossible to know where your money goes, which often leads to overspending and debt accumulation.

Practical Example: Consider Emma, a young professional earning $3,000 a month. By listing her expenses such as rent ($900), utilities ($150), groceries ($300), transportation ($200), and discretionary spending ($400), she can easily spot areas where she can save. If Emma manages to reduce eating out expenses by half, she saves $200 monthly, which can go towards paying off debt or building an emergency fund.

Budgeting Tools Comparison Table

| Budgeting Tool | Cost | User Friendliness | Features | Best For |

|---|---|---|---|---|

| Mint | Free | High | Automatic expense tracking, alerts | Beginners, casual users |

| YNAB (You Need A Budget) | $14.99/month | Medium | Goal-setting, debt payoff modules | Serious budgeters |

| Excel/Google Sheets | Free | Variable | Fully customizable | DIY enthusiasts |

The choice of budgeting tools depends on your personal preferences and financial goals, but regardless of the tool, the principle remains: track your income and expenses religiously. Budgeting is foundational because it promotes mindfulness and control, which are crucial for financial stability.

—

Credit and Debt Management: Navigating Borrowing Responsibly

Credit is a powerful financial tool but one that can lead to serious trouble if mismanaged. Understanding how credit works, the importance of credit scores, and responsible debt use are vital components of financial literacy.

Credit scores, which range from 300 to 850, measure your creditworthiness and affect your ability to borrow money or qualify for favorable interest rates. According to Experian’s 2023 data, the average U.S. credit score is approximately 711, considered “good.” A higher credit score can save thousands in interest over time.

Real Case: John, a recent graduate, took out student loans and began using a credit card without tracking his spending. His credit utilization soared over 90%, negatively impacting his credit score. With a poor credit score, John found it difficult to secure a car loan with a reasonable interest rate, ultimately paying more than twice as much over five years than if he had managed his credit responsibly.

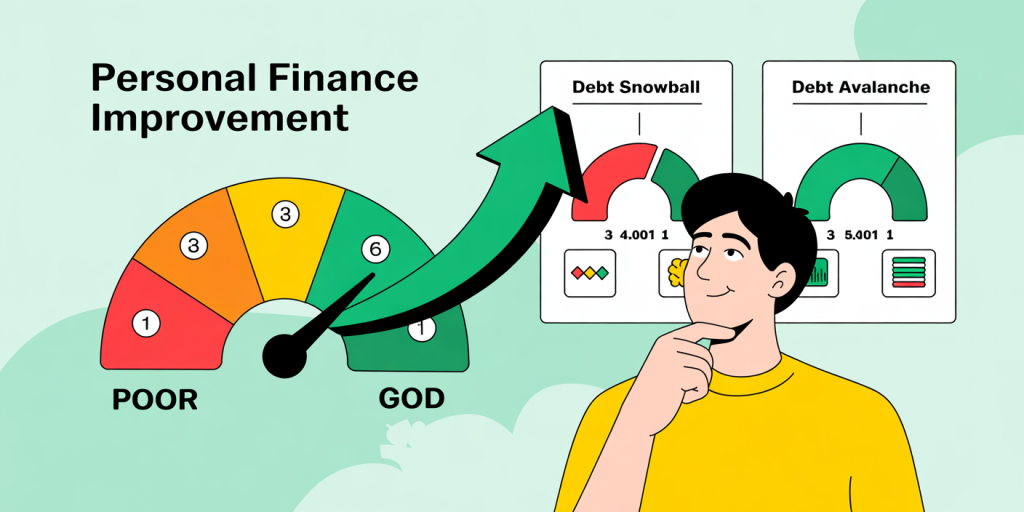

To avoid this, beginners should strive to maintain credit utilization below 30%, make payments on time, and avoid borrowing beyond their means. Debt management strategies such as the “Debt Snowball” or “Debt Avalanche” methods can also help systematically reduce outstanding debts.

Debt Repayment Strategy Comparison

| Strategy | Description | Pros | Cons |

|---|---|---|---|

| Debt Snowball | Pay smallest debts first, then roll payment to the next | Provides quick motivation boosts | Might cost more interest overall |

| Debt Avalanche | Pay debts with highest interest first | Saves more money on interest | Takes longer for initial wins |

Choosing the right approach depends on personality and financial goals, but the critical takeaway is that debt needs proactive management to protect your financial health.

—

Saving and Investing: Building Long-Term Financial Security

While saving is about setting aside money for future use or emergencies, investing involves using that money to generate additional income, often by purchasing assets like stocks or bonds.

For beginners, opening a high-yield savings account is a practical start. According to Bankrate’s 2024 report, the average high-yield savings account offers an interest rate of around 4%, significantly higher than conventional bank savings accounts. Consistent saving—even small amounts—can accumulate substantially over time due to compound interest.

On the investment side, beginners can take advantage of diversified mutual funds or low-cost ETFs (Exchange-Traded Funds). For example, the S&P 500 ETF has provided an average annual return of roughly 10% historically. Investing regularly through automatic contributions (dollar-cost averaging) helps mitigate market volatility.

Practical Example: Sarah started investing $200 monthly in a diversified ETF at age 25. By age 55, assuming an average return of 8%, her investment would grow to approximately $182,000, demonstrating the power of compound growth.

Savings vs. Investing: A Key Comparison

| Aspect | Saving | Investing |

|---|---|---|

| Risk | Low, funds typically insured | Varies, subject to market fluctuations |

| Liquidity | High, easy access | Moderate, can sell but may face losses |

| Purpose | Emergency funds, short-term goals | Wealth accumulation, retirement |

| Average Returns | 1-4% annually (based on rates) | 6-10% historically (stocks/bonds) |

Understanding the distinction between saving and investing helps set realistic financial goals and expectations, crucial for sustainable wealth building.

—

Protecting Wealth: Insurance and Emergency Preparedness

Having insurance and an emergency fund are critical components to safeguard against unforeseen events that can severely impact your finances. Many people overlook this until it’s too late.

According to a 2023 report by the Insurance Information Institute, only 65% of U.S. households have adequate health insurance, and many are underinsured when it comes to property or life insurance. The lack of insurance exposes individuals to risk that could dissolve years of financial planning.

An emergency fund, ideally covering 3-6 months of essential expenses, offers a buffer against job loss, medical emergencies, or urgent repairs. For example, Lisa lost her job unexpectedly but was able to cover her mortgage, utilities, and groceries for four months without borrowing, thanks to her emergency savings. Without this fund, she might have had to accumulate high-interest debt or sell investments prematurely.

Proper insurance coverage—health, auto, home, and life—combined with a solid emergency fund, completes a beginner’s financial safety net.

—

Looking Ahead: The Future of Financial Literacy and Its Impact

As financial products and technologies evolve rapidly—with innovations like digital wallets, cryptocurrencies, and robo-advisors—financial literacy will become increasingly important for navigating new challenges and opportunities. According to a 2024 survey by Deloitte, 72% of millennials believe financial education should be integrated into school curricula, reflecting a growing demand for systemic financial literacy initiatives.

Moreover, emerging technologies can provide personalized financial advice and automation, making it easier for beginners to manage their money effectively. However, foundational knowledge remains irreplaceable in critically assessing risks and benefits.

In the coming decade, enhanced financial education programs, accessible digital platforms, and increasing awareness will likely reduce financial exclusion and promote wealth equality. Developing financial literacy today is investing in a more secure and confidently managed financial future.

—

Building financial literacy is a marathon, not a sprint. Starting with the basics—budgeting, understanding credit, saving and investing wisely, and protecting your assets—lays the groundwork for lifelong financial success. By taking proactive steps and leveraging resources, beginners can turn financial uncertainty into empowerment. With continuous learning and adaptability, mastering personal finance is an achievable and rewarding journey.